Year-End Compliance Checklist for Indian Businesses (FY26-27)

Missing year-end compliance in India isn't just an administrative hassle— it's a massive financial risk. From the October 31 ITR audit deadline to the ₹100/day ROC late fees, founders must ruthlessly track GST, Tax, MCA, and Labour filings. Engage a Virtual CFO before March 31 to avoid the scramble and prevent Section 43B(h) and Rule 42 disallowances.

What Year-End Compliance Means in India

In India, year-end compliance refers to the mandatory regulatory filings a business must execute to close the Financial Year (April 1 to March 31). It spans four critical pillars: Income Tax (Advance Tax & ITR), GST (Annual Returns & Reconciliations), Ministry of Corporate Affairs (ROC filings), and Labour Laws (PF/ESI). While the financial year ends in March, the actual filing deadlines cascade throughout the calendar year up to December 31.

In my experience advising tech founders and SMEs, missing these deadlines usually results from fragmented communication between the founder, the accountant, and the CA.

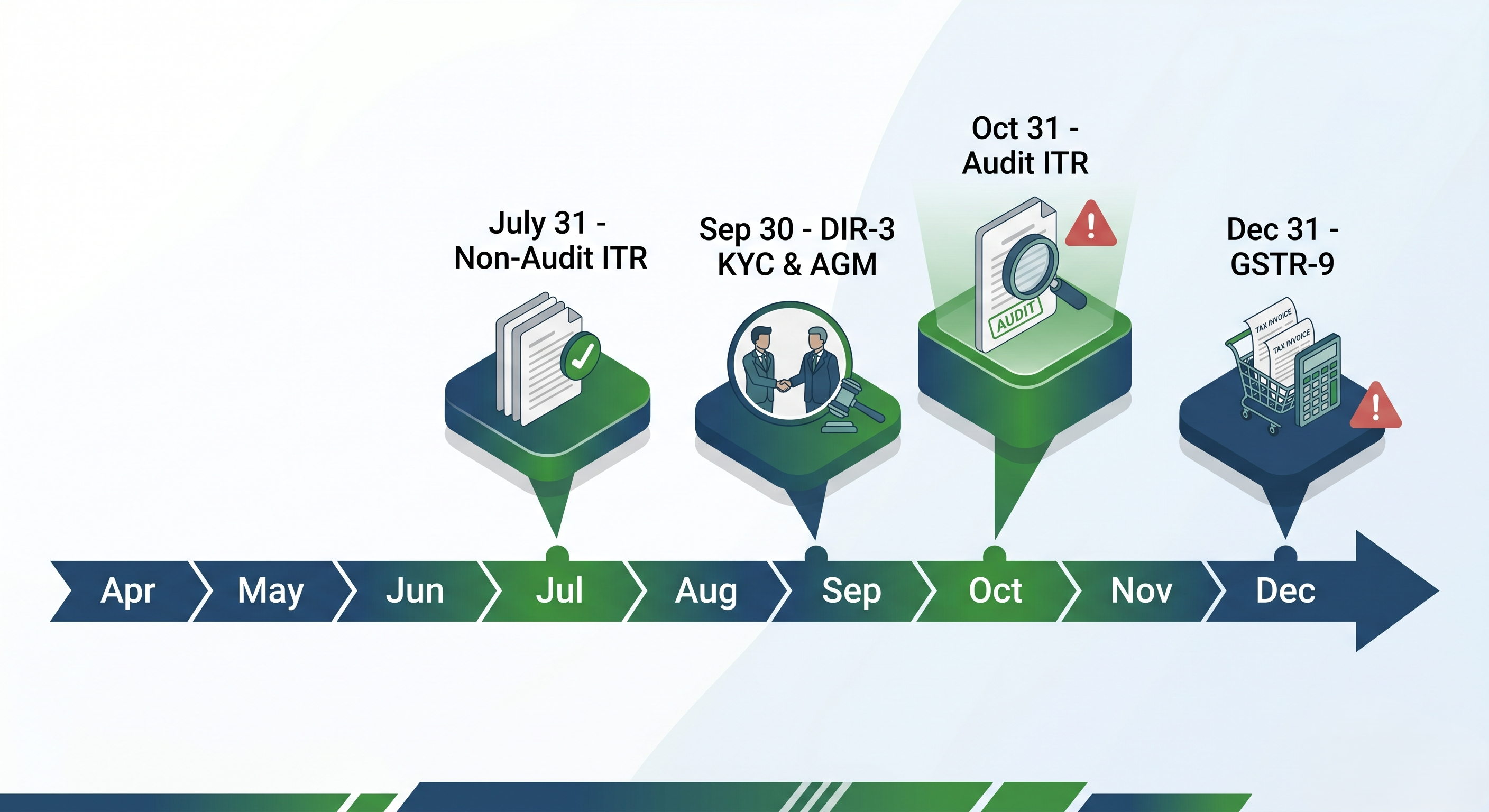

The Master Deadline Table: GST, ITR, ROC, TDS, Labour (FY26-27)

As financial consultants, we ensure our clients print and track this exact table.

Compliance Type | Form / Section | Frequency | FY26-27 Deadline | Penalty for Delay |

|---|---|---|---|---|

GST | GSTR-1 & GSTR-3B | Monthly | 11th & 20th of next month | ₹50/day (₹20 for Nil) |

GST Annual | GSTR-9 & 9C | Annual | Dec 31, 2027 | 0.25% of turnover |

Income Tax | ITR (Non-Audit) | Annual | Jul 31, 2027 | ₹5,000 (Sec 234F) |

Income Tax | ITR (Audit Cases) | Annual | Oct 31, 2027 | ₹5,000 (Sec 234F) |

ROC / MCA | AOC-4 (Financials) | Annual | 30 days post-AGM | ₹100/day |

ROC / MCA | MGT-7 (Annual Rtn) | Annual | 60 days post-AGM | ₹100/day |

Director KYC | DIR-3 KYC | Annual | Sep 30, 2027 | ₹5,000 + DIN block |

TDS | Form 26Q / 24Q | Quarterly | 31st of following month | ₹200/day (Sec 234E) |

Labour | PF & ESI | Monthly | 15th of next month | 12%-25% interest |

GST Year-End: Reconciliations, GSTR-9 & 9C, ITC Reversals

The GST framework is unforgiving if your books don't match the portal. You must execute a 3-way reconciliation between your accounting software, GSTR-2A/2B, and GSTR-3B before the final March filing.

Ineligible ITC: Reverse any Input Tax Credit (ITC) claimed on blocked items under Section 17(5) (e.g., employee cab services, food, club memberships).

GSTR-9 and 9C: If your aggregate turnover exceeds ₹2 Crore, filing GSTR-9 is mandatory. If it exceeds ₹5 Crore, you also need the GSTR-9C reconciliation statement certified by a professional.

Rule 42/43 Reversals: If you supply both taxable and exempt goods, year-end is the time to accurately calculate and reverse proportionate ITC.

Income-Tax Year-End: ITR, Tax Audit, Advance Tax, TDS True-Up

The Income Tax Department has tightened its data analytics. Everything you declare must match your AIS (Annual Information Statement).

Tax Audit Applicability: Under Section 44AB, a tax audit is mandatory if your turnover exceeds ₹1 Crore (cash basis) or ₹10 Crore (if 95%+ transactions are digital).

Advance Tax (March 15): 100% of your estimated tax liability must be paid by March 15. Shortfalls trigger 1% monthly interest under Section 234B and 234C.

Form 26AS vs. Books: Before closing the books, ensure all TDS deducted by your clients reflects in your Form 26AS. If not, chase the client to file their TDS returns.

ROC / MCA Annual Filings: AOC-4, MGT-7, DIR-3 KYC, ADT-1

For Private Limited Companies, the Ministry of Corporate Affairs (MCA) mandates strict corporate governance.

Board Meetings: Section 173 requires a minimum of 4 board meetings per year, with a maximum gap of 120 days between two meetings.

Annual General Meeting (AGM): Section 96 mandates that the AGM must be held by September 30.

Filings: AOC-4 must be filed within 30 days of the AGM, and MGT-7 within 60 days. Missing these attracts a flat late fee of ₹100 per day per form.

Auditor Appointment (ADT-1): Ensure your statutory auditor is appointed/re-appointed properly.

Payroll & Labour Compliance Year-End: PF, ESI, PT, Form 16

Labour compliance isn't just an HR issue; it directly impacts your P&L if disallowed.

PF & ESI: The Employees' Provident Fund Organisation (EPFO) requires strict monthly remittances by the 15th. Any delay means the employer contribution is disallowed as an expense under the Income Tax Act.

Form 16: Must be issued to all employees by June 15 for the TDS deducted on their salary.

Bonus & Gratuity: Ensure you have provisioned for the Payment of Bonus Act and Gratuity Act in your March 31 balance sheet.

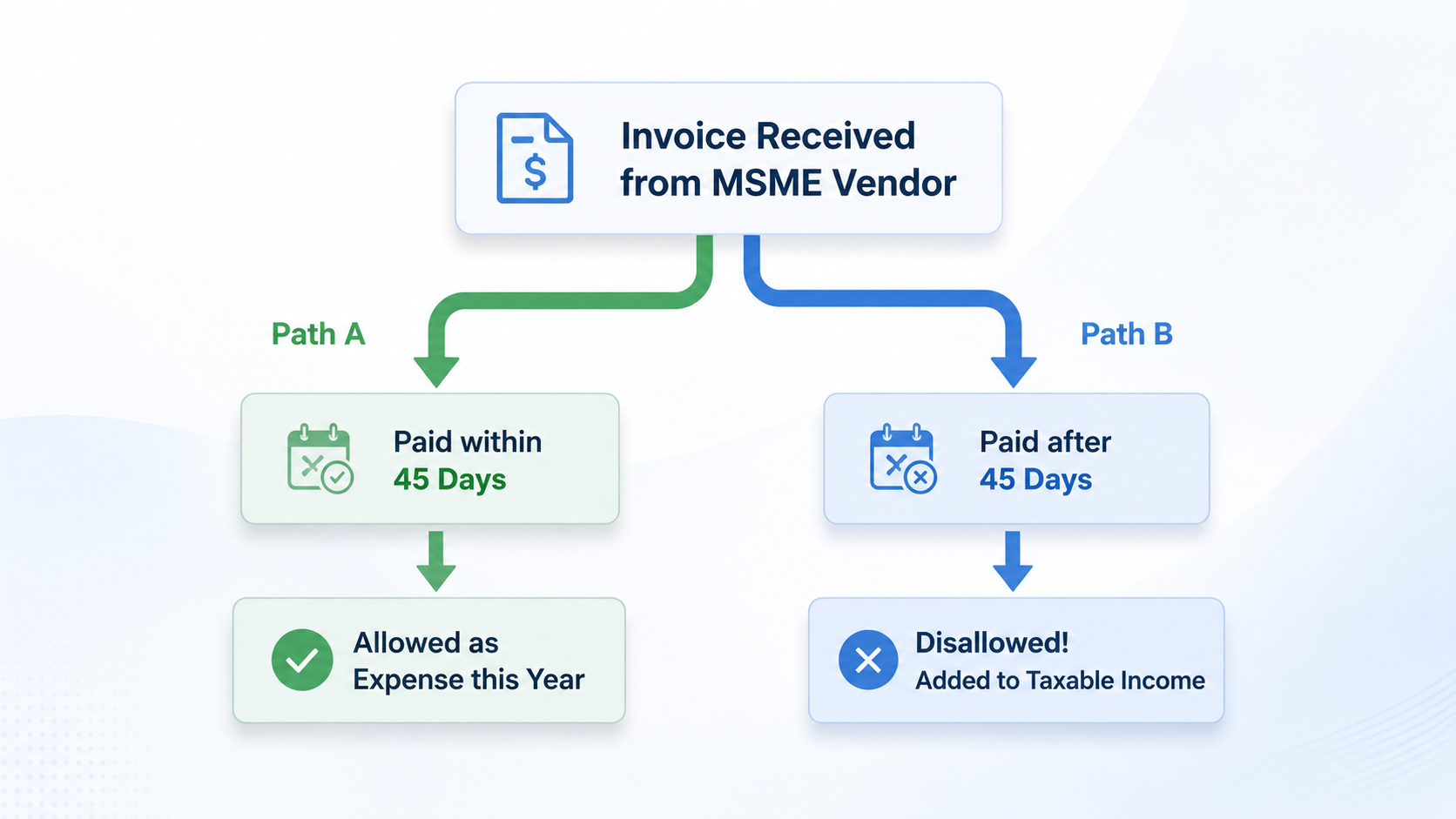

MSME-Specific Compliance: Form MSME-1, Udyam Updates, Sec 43B(h)

Our data shows that startups are routinely caught off-guard by the new MSME payment rules.

Section 43B(h): If you purchase goods or services from a registered Micro or Small Enterprise and delay payment beyond 45 days (with a written agreement) or 15 days (without one), that expense is disallowed in the current year. You will have to pay tax on it and can only claim it in the year the payment is actually made.

Form MSME-1: This is a half-yearly return filed with the ROC detailing all outstanding dues to MSME vendors that have exceeded 45 days.

Sector-Specific Year-End Items: NBFC, Trust, Section 8, LLP

Don't assume a standard private limited checklist applies to all entities:

LLPs: Must file Form 11 (Annual Return) by May 30 and Form 8 (Statement of Accounts) by October 30.

FDI / ODI Companies: Must file the FLA (Foreign Liabilities and Assets) return with the RBI by July 15.

Trusts & Section 8: Required to file Form 10B/10BB for their specialized tax audits.

Penalty Map: What Each Missed Filing Actually Costs

If you think a Virtual CFO is expensive, look at the cost of non-compliance:

GSTR-9: 0.25% of turnover (which can mean lakhs of rupees for a growing SME).

DIR-3 KYC: ₹5,000 fine and your Director Identification Number (DIN) gets deactivated, preventing you from signing any ROC documents.

TDS Returns (26Q/24Q): Section 234E levies a harsh ₹200 per day penalty.

ROC Forms (AOC-4/MGT-7): ₹100 per day, accumulating endlessly until filed.

Year-End Documentation: 12 Files Your CA Will Ask For

To avoid the last-minute scramble, consolidate these files in a single cloud drive before April 15:

Bank Statements (April to March)

Trial Balance & Ledgers

GSTR-1 and GSTR-3B Archive

TDS Challans

Updated Fixed Asset Register (FAR)

Payroll & Salary Registers

Vendor/Rent Agreements

Board Meeting Minutes Book

ESOP Register (if applicable)

Related Party Transactions (RPT) Register

Share Issue/Cap Table Paperwork

RBI / FEMA Filings (if foreign funding was received)

To properly execute all 12 items, we strongly recommend implementing robust cash flow management practices early in the year.

Key Takeaways

Start Reconciling in February: Waiting until March 31 to match GSTR-2B with your books guarantees ITC leakage.

Audit Your Payables: Section 43B(h) will permanently inflate your tax bill if you hold onto MSME vendor payments past 45 days.

The ₹100/Day Trap: ROC late fees compound daily. Prioritize your AGM and the subsequent AOC-4/MGT-7 filings.

Centralize Data: Whether you use a full-time finance head or outsource your compliance, having all 12 core documents centrally organized is the key to a fast, painless audit.

FAQs

Missing the December 31 deadline for GSTR-9 attracts a late fee of ₹200 per day (₹100 CGST + ₹100 SGST), capped at 0.25% of your turnover in the state.

Yes, you can file a belated or revised return under Section 139(4) or 139(5) until December 31 of the assessment year, but it attracts a ₹5,000 penalty under Section 234F.

Yes, every individual holding a DIN as of March 31 must file DIR-3 KYC by September 30, regardless of whether the company is active or inactive.

Dormant companies must file Form MSC-3 (Return of Dormant Company) instead of AOC-4, to retain their dormant status under the Companies Act.

No, the Section 43B(h) disallowance for delayed MSME payments currently only applies to payments made to micro and small enterprises operating as manufacturers or service providers, not retail or wholesale traders.

Section 8 (NGO/NPO) companies must file Form 10B/10BB under the Income Tax Act for audit, and must adhere to strict restrictions on dividend declarations compared to standard private limited companies.

Your trusted partner for all your Financial needs.

Finance Management

Strategic Services