FY26-27 Financial Planning Playbook for Indian SMEs

The success of FY26-27 is decided in April. Founders must immediately lock in their tax regime declaration (Sec 115BAC vs Old), provision for the MSME 45-day payment rule (Sec 43B(h)), and build a 13-week rolling cash flow model to survive capital winters.

FY26-27 in One Sentence: What Indian Founders Must Lock by April 30

Within the first 30 days of the new fiscal year (April 1 to April 30), Indian founders must declare their TDS tax regime, pass the final March 31 closing entries (including depreciation and MSME provisioning), reconcile GSTR-2B, establish a board-approved budget, and deploy a monthly KPI dashboard.

In my experience advising Indian SMEs, founders who treat April as a "slow month" spend the rest of the year fighting cash flow fires instead of scaling.

Close FY25-26 Properly: 7 Entries Most Founders Miss

Before planning the new year, you must cleanly close the old one. These 7 entries are heavily scrutinized by the Income Tax Department:

Section 32 Depreciation: Ensure block-of-assets calculations are applied to all capex.

Prepaid/Accrual Cutoffs: Allocate software subscriptions bridging March-April correctly.

GST Reverse Charge Mechanism (RCM): Pay and claim RCM for March vendor invoices.

TDS True-Up: Match your books precisely with Form 26AS/AIS.

Section 43B(h) MSME Provisioning: Disallow expenses for MSME vendors unpaid beyond 45 days.

ESOP Charge: Book the non-cash ESOP expense under Ind AS 102.

Leave Encashment: Provision for accrued employee leave balances.

FY26-27 Tax Regime Decision: New vs Old Slabs

Founders must decide the TDS deduction structure for their own salaries and inform HR by mid-April.

New Regime (Sec 115BAC): Now the default. It offers a Section 87A rebate making income up to ₹7 Lakhs effectively tax-free, but it removes standard deductions like HRA, LTA, and Section 80C.

Old Regime: Still beneficial if you have a massive home loan interest claim (Section 24b) combined with fully maxed out 80C, 80D (Health Insurance), and heavy HRA.

Tip: You must file Form 10-IEA if you have business income and wish to opt out of the new default regime.

Build the FY26-27 Budget: Bottom-Up P&L for Indian SMEs

Do not just copy last year's numbers + 15%. Build a bottom-up P&L.

Gross Margin Targets: SaaS should target 70%+, D2C brands 35-50%, and IT services 40-55%.

Opex Line-by-Line: Separate fixed costs (rent, base payroll) from variable costs (marketing CAC, cloud hosting).

Tax Provisioning: Year-end compliance requires cash. Set aside 25.17% of projected profits monthly into a separate current account for advance tax.

Cash-Flow & Runway Model: 13-Week + Annual View

Indian banks and VCs demand extreme capital efficiency. A Virtual CFO will typically build two models:

The 13-Week Cash Forecast: A granular, week-by-week spreadsheet tracking exactly what cash comes in (receivables) and goes out (payroll, vendor payouts) over the next quarter.

The Working Capital Cycle: Track your DSO (Days Sales Outstanding) minus DPO (Days Payable Outstanding). If your DSO exceeds 60 days, you are essentially providing free financing to your clients.

Tax & Compliance Calendar for FY26-27: April-March Deadlines

Print this out and stick it on your wall:

April: Tax regime declarations, GSTR-1 (11th).

June 15: Form 16 issuance + Q1 Advance Tax (15%).

July 15: FLA return for foreign-funded startups.

September 30: DIR-3 KYC + AGM deadline.

October 31: ITR filing deadline for audit cases.

November 29: MCA Form MGT-7 filing.

December 31: GSTR-9 Annual Return.

March 15: Q4 Advance Tax (100% cumulative).

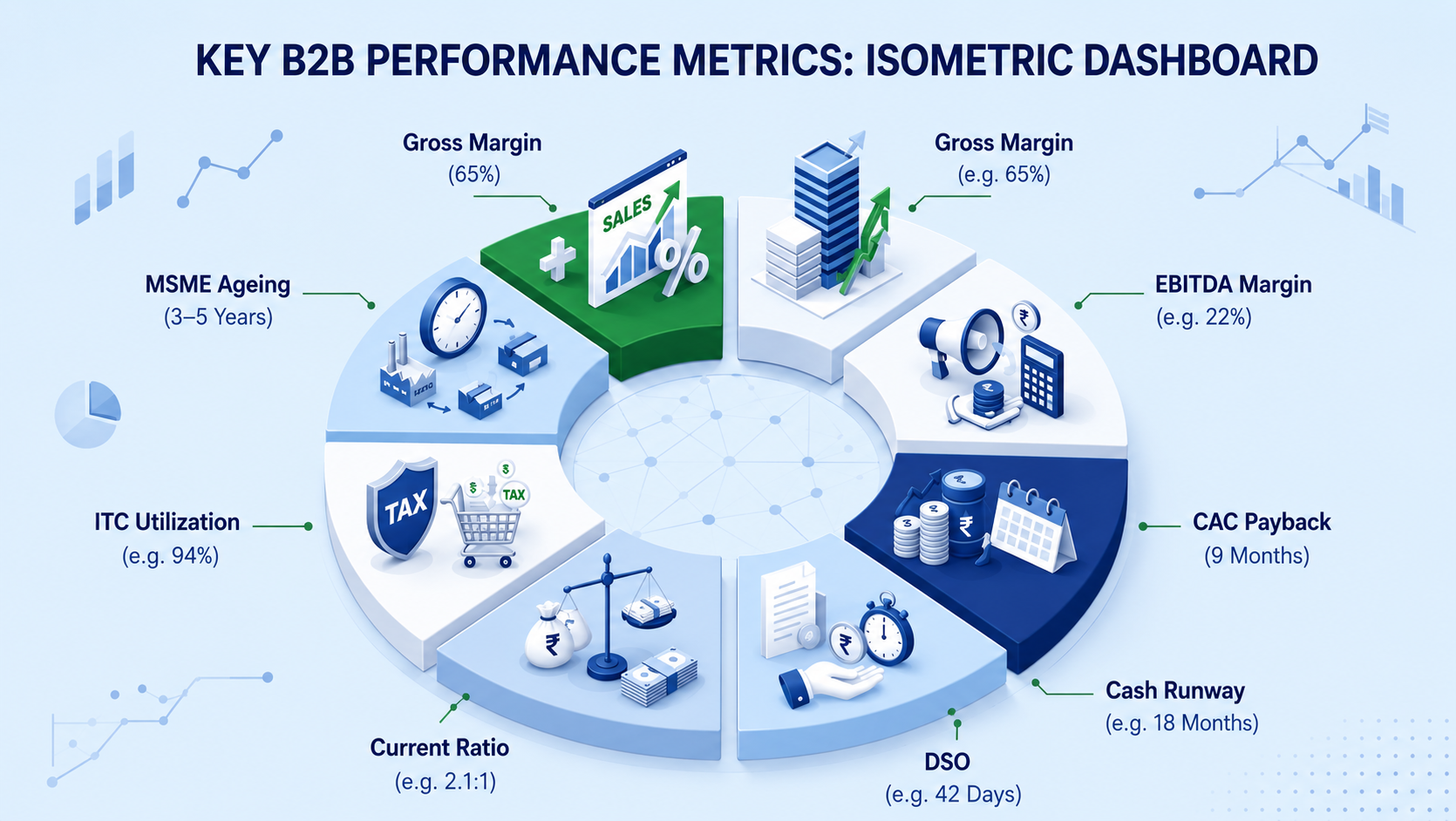

Pick 8 KPIs to Track Monthly: Targets for Indian MSMEs

Your MIS (Management Information System) should highlight these 8 metrics:

Gross Margin % (Is your core product profitable?)

EBITDA Margin (Target 10-25% depending on sector maturity)

CAC Payback (Target < 18 months)

Cash Runway (Target > 12 months)

DSO / Receivables Ageing (Target < 60 days)

Current Ratio (Target > 1.5x)

GST ITC Utilization %

MSME Ageing > 45 Days (To prevent Section 43B(h) penalties)

Capex & Tech Investments: Eligible Schemes

If you plan to buy machinery, servers, or office space in FY26-27, utilize Indian government schemes:

Section 35AD: 100% capex deduction for specified businesses (e.g., cold chain, hospitals).

Credit Guarantee (CGTMSE): Get collateral-free working capital or capex loans up to ₹5 Crore from SIDBI or major banks.

Accelerated Depreciation: Buy assets before September 30 to claim the full 100% of the allowable depreciation block, rather than the 50% half-year rule.

Risk & Insurance Refresh: What to Renew Before April 30

Insurance is often the last thing founders think about, until disaster strikes.

D&O (Directors & Officers) Insurance: Mandatory if you have VC board members.

Cyber Insurance: Crucial this year due to massive penalties introduced by the new DPDP (Digital Personal Data Protection) Act 2023.

Group Health: Review your premiums; expect a 10-15% medical inflation creep this year.

First 30 Days of FY26-27: A Day-by-Day Founder Checklist

Day 1-5: Circulate tax regime declaration forms to all employees. Rotate passwords on the GST Portal and MCA.

Day 6-15: Lock all March closing entries. Run payroll using new TDS slabs.

Day 16-25: Finalize the AOP (Annual Operating Plan) and present the bottom-up budget to the board for approval.

Day 26-30: Deploy the new automated MIS dashboard for the team.

Key Takeaways

Decide Tax Regimes Now: Sec 115BAC is the default. Do the math to see if the old regime's 80C/HRA benefits outweigh the new regime's standard ₹7L tax-free threshold.

Protect the 45-Day Limit: Section 43B(h) will destroy your tax planning if you habitually delay MSME vendor payments.

13-Week Cash is King: Build a rolling 13-week cash flow model immediately. Annual budgets are theoretical; weekly cash flow is reality.

Insure the Data: Buy cyber insurance this April to hedge against the severe penalties of the new DPDP Act.

FAQs

Yes, a budget is a living document. We recommend an AOP (Annual Operating Plan) review at the end of Q2 (September 30) to reallocate unspent budgets or adjust runway based on actual H1 revenue.

Do not wait until December. GSTR-9 (Annual Return) reconciliations should begin in April by auditing your GSTR-2B vs. books for the previous financial year to catch ineligible ITC claims early.

Yes, if your turnover crosses ₹2 Cr to ₹10 Cr, a Virtual CFO can build your 13-week cash flow models and KPI dashboards at a fraction of the cost of a full-time finance head.

Under Section 44AB, if 95% or more of your business receipts and payments are digital (non-cash), the tax audit threshold is elevated to ₹10 Crore turnover. Otherwise, it is ₹1 Crore.

Your trusted partner for all your Financial needs.

Finance Management

Strategic Services